Content

Paid-in capital is the amount of money that investors have put into the company. Retained earnings are the profits the company has generated over time that have not been paid out as dividends to shareholders. SE is an important measure of a company’s financial health because it represents the funds available to creditors and investors in the event of a liquidation.

Advisory services provided by Carbon Collective Investment LLC (“Carbon Collective”), an SEC-registered investment adviser. Go a level deeper with us and investigate the potential impacts of climate change on investments like your retirement account. This is the date on which the list of all the shareholders who will receive the dividend is compiled. To record this as a journal entry, we will debit the earnings account and credit the dividends payable account. Adam Hayes, Ph.D., CFA, is a financial writer with 15+ years Wall Street experience as a derivatives trader. Besides his extensive derivative trading expertise, Adam is an expert in economics and behavioral finance.

What is the Statement of Changes in Equity?

There is much to consider when creating a stockholders’ equity statement, like different types of stock and any additional gains or losses. While calculating these amounts, you’ll want to ensure not to leave any of these details out of the equation. This helps companies better understand how their investments are performing, and if any changes should be made to spark an increase. It will also help you attract potential investors to your business, especially if your balance continues to rise at a steady rate. Because shareholders’ equity experiences frequently change, however, it is crucial to review this information on a regular basis so you understand how to adapt and move forward.

- Before the statement of changes in equity can be prepared, the income statement must precede.

- The following statement of changes in equity is a very brief example prepared in accordance with IFRS.

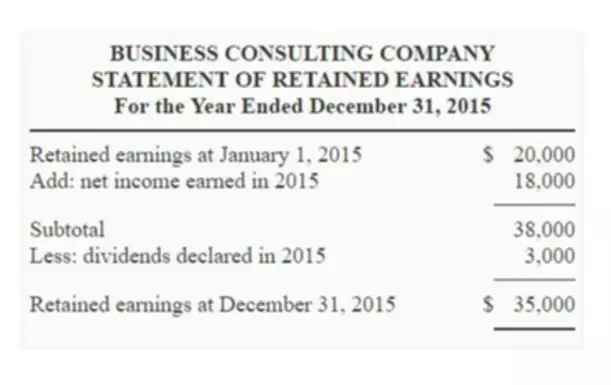

- Retained Earnings can be used for funding working capital, fixed asset purchases, or debt servicing, among other things.

- Our guide will both define and explain the components of a stockholders’ equity statement.

- Treasury shares can always be reissued back to stockholders for purchase when companies need to raise more capital.

- Once you define and outline this information, you’ll better understand your company’s financial wellbeing and performance, and how investors are viewing your potential.

It is one of the four financial statements that need to be prepared at the end of the accounting cycle. At some point, accumulated retained earnings may exceed the amount of contributed equity capital and can eventually grow to be the main source of stockholders’ equity. For this reason, many investors statement of stockholders equity view companies with negative shareholder equity as risky or unsafe investments. Shareholder equity alone is not a definitive indicator of a company’s financial health. If used in conjunction with other tools and metrics, the investor can accurately analyze the health of an organization.

Presentation of the Statement of Changes in Equity

Information regarding the par value, authorized shares, issued shares, and outstanding shares must be disclosed for each type of stock. If a company has preferred stock, it is listed first in the stockholders’ equity section due to its preference in dividends and during liquidation. The statement of shareholders’ equity (SSE) is a financial statement that shows the changes in a company’s equity over a period of time. The statement of cash flows (SCF) is a financial statement that shows how changes in a company’s cash and cash equivalents have affected its financial position over a period of time.